Usual Response To Home Mortgage Questions

Content writer-Huynh SalomonsenAre you looking for information on home mortgage information? There is a lot to know when it comes to home loans. Regardless of what brought you here, it is possible for everyone to get some useful home loan information from this article.

Organize your financial life before going after a home mortgage. If your paperwork is all over the place and confusing, then you'll just make the entire mortgage process that much longer. Do yourself and your lender a favor and put your financial papers in order prior to making any appointments.

Why has your property gone down in value? The home may look the same or better to you, but the bank has an entirely different view.

Work with your bank to become pre-approved. Pre-approval helps give you an understanding of how much home you can really afford. It'll keep you from wasting time looking at houses that are simply outside of your range. It'll also protect you from overspending and putting yourself in a position where foreclosure could be in your future.

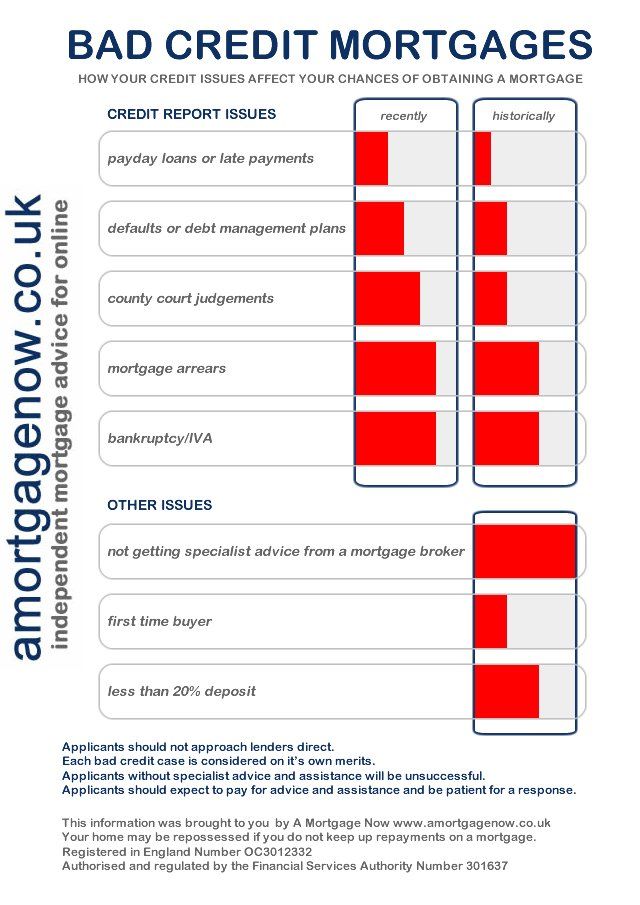

Some creditors neglect to notify credit reporting companies that you have paid off a delinquent balance. Since your credit score can prevent you from obtaining a home mortgage, make sure all the information on your report is accurate. You may be able to improve your score by updating the information on your report.

If you can afford a higher monthly payment on the house you want to buy, consider getting a shorter mortgage. read here are based on a 30-year term. A mortgage loan for 15 or 20 years may increase your monthly payment but you will save money in the long run.

Once you have chosen the right loan for your needs and begun the application process, make sure to get all of the required paperwork in quickly. Ask for deadlines in writing from you lender and submit your financial information on time. Not submitting find out this here on time may mean the loss of a good interest rate.

If you are having difficulty refinancing your home because you owe more than it is worth, don't give up. New programs (HARP) are in place to help homeowners out in this exact situation, no matter how imbalanced their mortgage and home value seems to be. Discuss a HARP refinance with your lender. If a lender will not work with you, go to another one.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Save up for the costs of closing. Though you should already be saving for your down payment, you should also save to pay the closing costs. They are the costs associated with the paperwork transactions, and the actual transfer of the home to you. If you do not save, you may find yourself faced with thousands of dollars due.

Never sign anything without talking to a lawyer first. The law does not fully protect you from the shrewd practices that many banks are willing to participate in. Having a lawyer on your side could save you thousands of dollars, and possibly your financial future. Be sure to get the right advice before proceeding.

Learn about the various types of home mortgage that are available. There are quite a few different kinds of home loans. There are different time frames, different payment schedules and different interest rates. You need to learn the pros and cons of each. Consult your lender regarding your personal mortgage options.

If you don't mind paying more on your mortgage payment, consider taking out a 15 or 20 year loan instead. These loans are shorter-term ones, and they have a higher monthly payment with an interest rate that's usually lower. You will save thousands of dollars by doing this.

Remember, no home mortgage is "a lock" until you've closed on the home. A lot of things can affect your home mortgage up to that point, including a second check of your credit, a job loss, and other types of new information. Keep your finances in check between your loan approval and the close to make sure everything goes as planned.

Be realistic when choosing a home. Just because your lender pre-approves you for a certain amount doesn't mean that's the amount you can afford. Look at your income and your budget realistically and choose a home with payments that are within your means. This will save you a lifetime of stress in the long run.

Ask around about mortgage financing. You may be surprised at the leads you can generate by simply talking to people. Ask your co-workers, friends, and family about their mortgage companies and experiences. They will often lead you to resources that you would not have been able to find on your own.

Pay off more than your minimum to your home mortgage every month. Even $20 extra each month can help you pay off your mortgage more quickly over time. Plus, it'll mean less interest costs to you over the years too. If you can afford more, then feel free to pay more.

Be prompt about getting your documentation to your lender once you have applied for a home mortgage. If your lender does not have all the necessary documentation on hand, and you have begun negotiations on a home, you could end up losing lots of money. Remember that there are nonrefundable deposits and fees involved, so you must get all your documentation submitted in a timely manner.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

Now that you are armed with the valuable information found in this article, you have a better chance of getting the financing you need. Your best option may be a short term loan that you can convert later, or a 30 year mortgage. Follow the advice in this article to find the loan that works best for you.